Your Financial Dream Team – The Financial Team That Actually Gets You to Financial Freedom

By David Samuel

Everyday Finance Coach

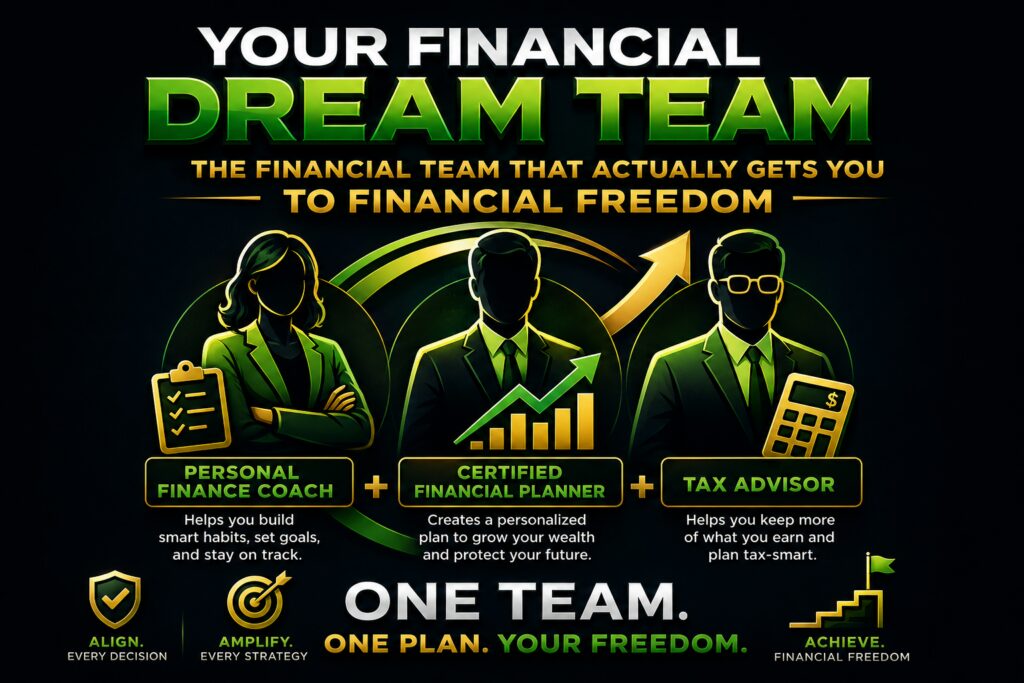

In my personal finance coaching practice, I’m often asked about the difference between what I do and what a financial planner does, and whether our roles are complimentary or redundant. The truth is that nobody builds financial freedom alone. Even the wealthiest people you can think of surround themselves with a team — not because they can’t read a balance sheet, but because financial freedom requires different kinds of expertise at different stages of the journey. If you’re serious about getting there, you need your own version of that team. It’s not a matter of choosing to work with a coach OR a planner. I believe that the dream team actually consists of three players who matter: a personal finance coach, a Certified Financial Planner (CFP), and a tax advisor.

If we were talking about your physical wellness, this same dream team (Coach, CFP, Tax Advisor) would be comprised of your personal trainer, your primary care physician and your cardiac surgeon. Each professional has a clear lane. Your trainer doesn’t diagnose heart disease or prescribe medication, just like your coach isn’t the one drafting intricate tax strategies. Your primary care doctor isn’t running your interval sprints, just as your CFP isn’t meeting with you every week to reset your spending habits. And when you need serious surgical expertise—whether in the operating room or in the tax code—you’re not calling your trainer or your generalist doctor; you’re turning to the specialist whose entire craft is built around that high‑stakes moment.

The Personal Finance Coach: Your Everyday Teammate

You can think of your finance coach as a personal trainer for your finances, the person who’s in the trenches with you week to week. As your personal finance coach, my job isn’t to pick your investments or file your taxes — it’s to help you build the habits, systems, and mindset that make every other financial decision easier. That means getting your budget under control, building a plan to pay off debt, creating savings and investment habits that actually stick, and having honest conversations about how money shows up in your relationships and decisions.

Coaching is behavioral work, not technical work. As a coach, my value is in the accountability and clarity that gets you organized enough to actually use the advice a financial planner or tax advisor gives you. A lot of people come to a CFP with messy numbers, no clear goals, and no follow-through system. Coaching fixes that first, so the technical advice you eventually get doesn’t just sit in a drawer.

The CFP: Your Technical Strategist

Once your habits are solid and your financial life has some complexity — a growing investment account, a home purchase, a retirement account rollover, an inheritance — you may need someone licensed to manage your investments and give you specific, personalized advice. That’s where a Certified Financial Planner comes in.

CFP professionals complete rigorous coursework, pass a comprehensive exam, and log thousands of hours of supervised experience before they earn the designation. More importantly, they’re bound by a fiduciary duty — a legal and ethical obligation to act in your best interest at all times when giving financial advice, not just when it’s convenient. That includes a duty of loyalty (your interests come before theirs), a duty of care (they must analyze your situation with real diligence), and a duty to follow your instructions. This is not the province of coaching, since it requires licensing, exams, and regulatory oversight that coaching doesn’t carry.

A good CFP builds your investment strategy, models your retirement income, helps structure your estate plan, and coordinates the moving pieces of a complex financial life. They’re the strategist who takes your goals and turns them into a specific, executable plan.

The Tax Advisor: Your Specialist

If the coach is your financial personal trainer and the CFP is your financial strategist, the tax advisor is your specialist — the person who makes sure the strategy doesn’t quietly get eaten alive by taxes. A CPA or enrolled agent understands the tax code at a depth that most financial planners don’t practice day to day, and they can catch things that materially change your bottom line: how a Roth conversion affects your tax bracket this year, how to time capital gains, how self-employment income should be structured, or how a windfall should be handled before December 31st instead of after.

Tax advisors are especially valuable at decision points: selling a business, receiving equity compensation, moving states, or navigating a major life change like marriage, divorce, or inheritance. Skipping this seat on the team is one of the most expensive mistakes people make, because tax decisions often can’t be undone after the fact.

How the Dream Team Works Together

Here’s the sequence I recommend to most people: start with coaching to get your cash flow, debt, and savings habits under control. As your financial life grows — more assets, more complexity, bigger decisions — bring in a CFP to build and manage the technical strategy. Loop in a tax advisor at key inflection points, and ideally have your CFP and tax advisor coordinating directly with each other.

None of these three roles compete with each other. A coach who tries to give tax advice is overstepping. A CFP who ignores behavior and habits will watch a beautiful plan fail because the client can’t execute it. And anyone who ignores taxes is leaving real money on the table. Financial freedom isn’t the result of one great advisor — it’s the result of the right people, in the right seats, at the right time.

If you’re not sure which seat you need filled first, that’s a great place to start a conversation. Most people need a coach before they need a planner, and a planner before they need a specialist — but wherever you are in that sequence, the goal is the same: build a team that moves you steadily toward financial freedom.

If you’re ready to make progress in your effort to take control of your finances, this is exactly the kind of work done with my coaching clients every day—clarifying priorities, creating a practical plan, and following through on it. If you’d like support with your own situation, you’re welcome to reach out anytime right here, or by email at david@everydayfinancecoach.com