Intentional Spending: How to Align Your Spending with What Actually Matters

By David Samuel

Everyday Finance Coach

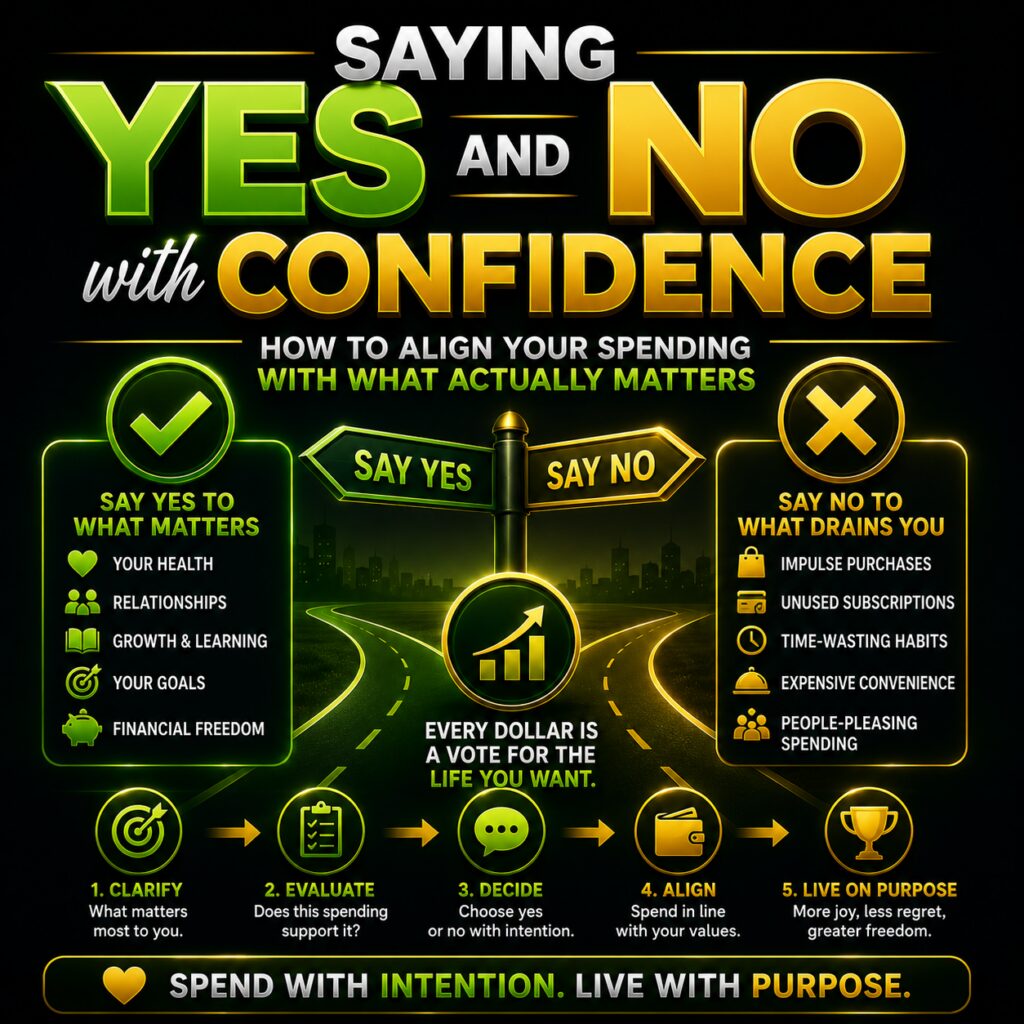

Most people don’t overspend because they’re reckless; they overspend because their money is saying “yes” to whatever’s in front of them instead of what actually matters most to them. Values‑based spending flips that around so your default “yes” and “no” start matching the life you want, not just the day you’re having. This isn’t about never buying coffee or cutting every joy. It’s about choosing your joys on purpose.

Step 1: Get Clear on What Actually Matters

You can’t align your spending with your values if you haven’t named those values. Start with a quick exercise:

- List 5–10 things that bring you the most meaning or satisfaction in life.

- For each, ask: “What value does this represent?”

- Examples: family, freedom, security, health, creativity, adventure, generosity, growth.

- Circle your top 3–5 values—the ones you’d be heartbroken to lose or live without.

Now look at your last month or two of spending and ask, in a big‑picture way: “Does this look like someone who values these things?” For most people, the answer is “sort of, but not really”—and that gap is where your new “yes” and “no” will come from.

Step 2: See Where Your Money and Values Don’t Match

Next, connect your values to your actual expenses. Take your recent spending and loosely sort it into four categories:

- Highly aligned: Clearly tied to your core values (for example, trips to see family, a class that grows your skills, therapy, giving).

- Somewhat aligned: Adds some value, but not essential.

- Neutral: Just the cost of being alive (utilities, basic groceries, insurance).

- Misaligned: You wouldn’t really miss it; it doesn’t support any value you care about.

A few examples:

- If you value health, your gym membership might be “highly aligned,” but frequent late‑night fast food might be “misaligned.”

- If you value freedom and security, building an emergency fund and investing are “highly aligned,” but impulse online shopping might not be.

- If you value relationships, spending on shared experiences may be aligned, while mindless solo scrolling/ordering might not be.

The goal isn’t to judge yourself; it’s to spot patterns. Where are you accidentally funding a life you don’t even want?

Step 3: Redefine What You’re Willing to Say “Yes” To

Once you see the patterns, you can start to consciously choose your “yes”. Ask for each major category of spending:

- “If I spent a little more here, would my life feel richer and more aligned?”

- “If I spent a little less here, would I really be worse off—or just slightly inconvenienced?”

Then:

- Explicitly decide a few things you’re happy to spend more on because they truly reflect your values.

Example: “Travel with my kids,” “Books and courses,” “Giving,” “Health.” - Pick some areas you’re willing to pull back on because they don’t really matter as much as you’ve been funding them.

Example: “Random Amazon purchases,” “Extra streaming services,” “Frequent delivery instead of planned meals.”

This is where many people discover they’re not “bad with money”—they’ve just never given themselves permission to let their budget look different from everyone else’s.

Step 4: Build a Simple Values‑Based Spending Plan

You don’t need a hyper‑detailed budget to live your values. You can create a simple structure that channels money where you want it to go.

A practical approach:

- Cover essentials first (housing, utilities, groceries, transportation, insurance, minimum debt).

- Decide on fixed amounts for future‑you priorities:

- Emergency fund and debt payoff (security/freedom)

- Investing for long‑term goals (independence, flexibility).

- Then divide the remaining “flex” money across a few value‑aligned categories you’ve chosen in advance

- For example: “Experiences,” “Health & Growth,” “Generosity,” “Fun”

You can even rename your budget categories to match your values:

- Instead of “Entertainment,” call it “Connection & Experiences.”

- Instead of “Misc,” call it “Joy Money.”

- Instead of “Savings,” call it “Future Freedom.”

Now you’re not just cutting or spending; you’re deliberately funding the life that matters to you.

Step 5: Use Small Scripts to Say No (and Yes) with Less Guilt

Even with a plan, real‑time decisions can be tricky. Quick scripts help you pause without overthinking. Before a non‑essential purchase, try asking:

- On a scale of 1–10, how aligned is this with my top values?

- If I say yes to this, what am I saying no to later?

- Will this still feel worth it next week?

You might adopt some phrases like:

- When saying no:

- This isn’t a bad purchase—it’s just not my priority right now.

- I’m choosing to put that money toward Future Freedom instead.

- When saying yes:

- This costs money, but it clearly supports Generosity, so I’m spending this with intention.

- I’m okay spending more here because it lines up with the life I’m trying to build.

You’re not trying to eliminate every impulse, just to introduce a brief moment of alignment before the money leaves.

Step 6: Revisit and Adjust as Life Changes

Values‑based spending is not a one‑time exercise. Your priorities will shift with new seasons—career changes, relationships, kids, health, or even just personal growth.

Once a quarter or a couple of times a year:

- Re‑list your top 3–5 values and see if anything has changed.

- Glance through a month of spending and ask, “Where does this still match?” and “Where has my money drifted?”

- Make one or two small tweaks—like increasing a value‑aligned category or cutting a misaligned one—rather than trying to overhaul everything.

Bit by bit, your financial life starts to feel less like a tug‑of‑war and more like a reflection of who you are and what you care about.

Here are four examples, each centered on a different core value.

Family First: Rewriting the Weekends

Meet Chad and Nicola (Value = Family & Connection)

Chad and Nicola realized that even though they said family was their top value, their money told a different story. A subscription audit and a quick look at their transactions showed a lot of solo impulse buying—apps, late‑night Amazon orders, and random takeout—while they kept saying, “We should plan something fun with the kids soon.”

They decided to make that mismatch explicit. On a money date, they wrote “Family & Connection” at the top of their budget and asked: “What does spending look like when that’s truly our priority?”

Changes they made:

- Canceled two streaming services and a couple of underused subscriptions, freeing up about 80/month.

- Capped solo convenience lunches and last‑minute takeout, redirecting another 100.

- Created a new “Family Days & Memories” category funded with that 180 every month.

Now, instead of defaulting to separate screens at home, they plan one intentional family activity every weekend—day trips, board game nights with special snacks, or outings to parks and free events. The total spend didn’t skyrocket; it just shifted.

The big impact: they stopped feeling guilty about spending on family time, because they’d clearly decided, “This is what we say yes to first.”

Freedom & Flexibility: Trading Stuff for Options

Meet Kayla (Value = Freedom & Independence)

Kayla was in her mid‑30s, earning decent money, but always felt boxed in—tied to a job she didn’t love, worried about emergencies, and frustrated that she wasn’t any closer to financial independence. Her top values list came out like this: Freedom, Security, Adventure.

Her spending, on the other hand, leaned heavily toward lifestyle creep: frequent online shopping “because it was a long day,” multiple ride‑shares a week instead of planning ahead, and a rotating cast of “treat” purchases that lost their shine quickly. She reframed her decisions around one question: “Is this purchase giving me more freedom, or taking it away?”

Changes she made:

- Cut back clothing and home décor spending by setting a simple rule: no more than one “non‑essential item” per month, and it had to be a 9 or 10 out of 10 want.

- Swapped frequent last‑minute ride‑shares and delivery fees for weekly batch errands and meal prep.

- Redirected roughly 350/month toward:

- Building a 3‑month emergency fund (security)

- Increasing automatic investments into a retirement account (future freedom).

Within a year, the emergency fund was fully stocked and Kayla’s investments were noticeably higher. That bolstered her confidence enough to explore a role change—and eventually negotiate a more flexible position. She didn’t get there by being perfect; she got there by consistently asking, “Does this support my freedom?”

Health & Energy: Aligning the Body with the Budget

Meet Cadence (Value = Health & Vitality)

Cadence kept saying, “My health is my priority,” but her money told a different story. She had an unused gym membership, constant food delivery, and very little left over each month for things that actually supported her physical and mental well‑being.

When she did the values exercise, Health, Growth, and Calm sat at the top of her list. That gave her a lens: “If health and calm are my values, where is my money supporting that, and where is it fighting against it?”

Changes she made:

- Canceled the fancy gym she never went to and joined a lower‑cost community gym much closer to home—saving 60/month and increasing the odds she’d actually go.

- Set a cap on food delivery and instead started a Sunday “prep hour” to make healthy, quick meals and snacks for the week.

- Reallocated some of the saved money toward:

- Weekly fitness classes she genuinely enjoyed (yoga and dance)

- A therapy session twice a month, which she’d been putting off “until money was better.”

Cadence’s total “health” spending didn’t necessarily go down—but it became highly aligned with her values instead of being random and guilt‑ridden. She actually felt good about those line items because they clearly supported how she wanted to feel in her body and mind.

Generosity & Impact: Giving Without Resentment

Meet Parker (Value = Generosity & Contribution)

Parker always said he wanted to give more, but there was a quiet tension: he’d donate spontaneously when asked, then feel stressed about money later and regret the amount. His values exercise surfaced Generosity, Community, and Faith as core priorities.

Looking at his bank statements, he saw very inconsistent giving and a lot of unplanned spending—small purchases that didn’t mean much individually but added up. He decided to turn generosity into a planned, joyful part of his spending instead of a guilt‑driven surprise:

- Chose a specific percentage of his income (starting small at 3–5%) to go toward giving each month.

- Set up automatic transfers into a “Giving” savings bucket so the money was ready when needs or opportunities arose.

- Reviewed his “neutral” and “misaligned” spending and trimmed enough to fund that giving without sabotaging his essentials or savings goals.

Now, when a friend runs a fundraiser, his community group supports a cause, or there’s a need at his local school, Parker can say yes without resentment, because generosity already has a permanent place in his budget. The result: he gives more consistently and feels better about it—and his other priorities (like emergency savings and debt payoff) are still on track because they’re all part of the same values‑based plan.

Your Call to Action

Which of these stories feels closest to where you are right now—Family, Freedom, Health, Generosity, or something else? What’s one small shift you could make this month so your spending lines up a little more with that value?

If you’re ready to make progress in your effort to take control of your finances, this is exactly the kind of work done with my coaching clients every day—clarifying priorities, creating a practical plan, and following through on it. If you’d like support with your own situation, you’re welcome to reach out anytime at david@everydayfinancecoach.com