From Overwhelmed to Organized: How to Build a Debt Payoff Plan That Sticks

By David Samuel

If your debt feels like a tangled knot—multiple accounts, different due dates, and a sense that you’re always behind—you’re not alone. The goal of a good payoff plan isn’t perfection; it’s having a clear, simple path you can actually follow for months and years, not days and weeks.

This post will take you from “I don’t even know where to start” to a concrete, realistic plan to pay off debt in a way that fits your real life.

Why Minimum Payments Keep You Stuck

Minimum payments are designed to protect the lender, not to help you get out of debt.

When you only pay the minimum:

- Most of your payment goes to interest, not principal.

- Your payoff timeline stretches into years (or decades).

- A single new purchase can undo months of progress.

For example, if you carry a few thousand dollars on a card at a high interest rate and only pay the minimum, you can easily pay back double (or more) of what you originally borrowed over time. The point isn’t to scare you—it’s to make it clear that minimum payments are the floor, not the plan.

Your goal: shift from “What’s the least I can pay?” to “What’s the most I can reasonably send without breaking my budget?”

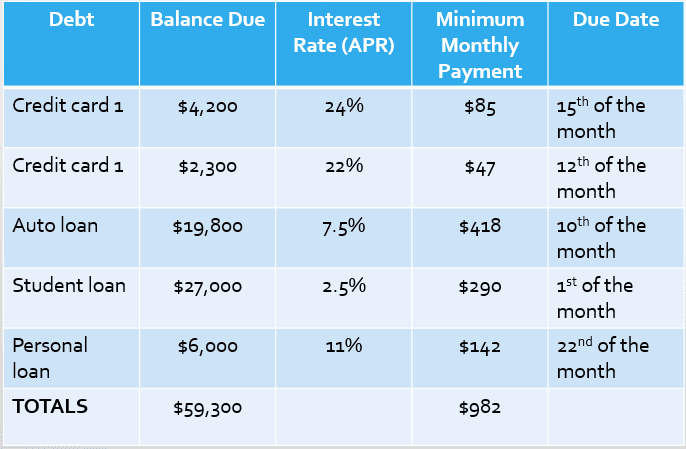

Step 1: Face the Numbers (Without Beating Yourself Up)

The first step is often the hardest: putting everything in one place. But once you do, the anxiety of the unknown starts to fade.

Grab a notebook or spreadsheet and list each debt:

- Lender or card name

- Current balance

- Interest rate (APR)

- Minimum monthly payment

- Due date

Include credit cards, personal loans, auto loans, student loans, store cards, and buy-now-pay-later plans.

Now add two totals:

- Total debt balance

- Total minimum payments per month

This is a snapshot of your debt inventory. You might feel a rush of emotion here—guilt, frustration, fear. That’s normal. The numbers haven’t changed just because you wrote them down. What has changed is that you now have a clear picture to work with. That alone is progress.

Step 2: Stop the Leak Before You Fix the Ship

You can’t build a lasting payoff plan if you’re still adding to the balances. For the next 30–60 days:

- Pause new charges on any card you’re trying to pay down.

- Delete saved cards from shopping sites and apps.

- Use debit or cash for everyday spending while you reset habits.

You’re not banning credit cards forever. You’re simply giving yourself space to turn the tide from “debt growing” to “debt shrinking.”

Step 3: Choose Your Payoff Strategy

Two main strategies work well. Both can succeed, so the best one is the one you’ll stick with.

Debt Snowball (Motivation First)

- List your debts from smallest balance to largest.

- Pay the minimum on all debts.

- Put any extra money (kick-start) you can find toward the smallest balance.

- When it’s paid off, roll its entire payment (payment + kick-start) into the next smallest balance.

You get quick wins. Seeing a balance hit zero builds momentum and makes you feel like, “I can actually do this.” If you’ve started and stopped payoff plans before and know you need fast progress you can feel, the Snowball approach may be your best bet.

Debt Avalanche (Math First)

- List your debts from highest interest rate to lowest.

- Pay the minimum on all debts.

- Put every extra dollar toward the highest-interest debt.

- When it’s paid off, roll its payment (payment + kick-start) into the next highest rate.

You pay less interest overall and usually become debt-free faster.

If you’re very numbers-driven, avalanche may appeal more. If emotional wins matter more, snowball might be the better fit. There’s no wrong answer—as long as you commit.

Step 4: Build a Realistic Monthly “Kick-Start”

To move beyond minimum payments, you need a kick-start—a specific amount you’ll put toward debt above your total minimums each month. Here’s how to find it:

- Add up your monthly take-home income.

- Subtract your essential expenses: housing, utilities, groceries, transportation, insurance, childcare, and other must-haves.

- Subtract the total of all minimum debt payments.

What’s left is the money available for lifestyle spending and extra debt payoff. Now decide, honestly, how much of that remainder can you commit to extra debt payments without constantly feeling deprived?

Maybe it’s $75, $150, or $400 a month. The key is: it has to be sustainable, not heroic. A modest amount you can keep sending month after month will beat an aggressive plan you abandon in three weeks. If your leftover amount is tiny or negative, look for quick adjustments:

- Cut or pause a few subscriptions.

- Trim dining out or convenience spending.

- Call and negotiate lower rates on bills where possible.

- Explore small, temporary income boosts: overtime, a side gig, selling unused items.

Step 5: Put Your Plan on Rails With Automation

Once you have your list of debts, your chosen strategy (snowball or avalanche), and your monthly kick-start, it’s time to automate as much as you can.

- Set minimum payments on autopay for every debt to avoid late fees and damage to your credit.

- Set an automatic extra payment to your current target debt (the smallest balance for snowball, highest rate for avalanche) right after your paycheck hits.

Automation helps your plan keep going even when you’re tired, stressed, or busy. You don’t have to remember to be disciplined; the system remembers for you. Whenever you get a windfall—tax refund, bonus, side income—consider sending a chunk to your current target debt. These lump sums can knock months off your timeline.

You can access a very powerful online tool to build your debt snowball/avalanche right here.

Step 6: Expect Obstacles—and Plan for Them

A payoff plan that sticks is not one that never gets disrupted; it’s one that has room for real life.

Build in resilience by:

- Keeping a small starter emergency fund (even $500–1,000) so every surprise doesn’t go straight onto a card.

- Accepting that some months will be better than others. A tight month doesn’t mean you’ve failed—it just means you adjust and keep going.

- Scheduling a 15-minute “money check-in” once a month to review progress and make small tweaks.

Think of this as a long, steady climb, not a sprint. You’re changing your trajectory, not chasing instant perfection.

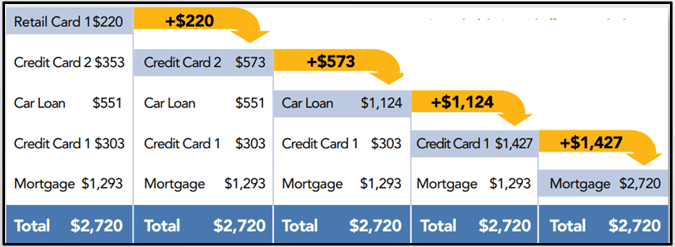

Step 7: Protect Your Progress as Debts Disappear

The most powerful moment in your plan is when one debt hits zero. That’s where many people accidentally drift back into old habits—or where you can supercharge your progress. When a debt is paid off, you keep paying the same total amount each month, but redirect it to your next target.

This is where momentum becomes transformation. The same monthly dollars that used to go to interest can start building your emergency fund, retirement accounts, and long-term goals.

Your Next Step: A 30-Minute Debt Clarity Session

If you’re overwhelmed, don’t try to do everything today. Start with this:

- Spend 30 minutes listing all your debts and totals.

- Choose snowball or avalanche.

- Decide on a realistic extra monthly amount.

- Set up one automatic extra payment to your top-priority debt.

You’ll go to bed knowing that, for the first time, you have a plan that doesn’t just live in your head—it’s actually in motion.

If you’re ready to make progress in your effort to take control of your finances, this is exactly the kind of work done with my coaching clients every day—clarifying priorities, creating a practical plan, and following through on it. If you’d like support with your own situation, you’re welcome to reach out anytime right here, or by email at david@everydayfinancecoach.com

{kind=link}